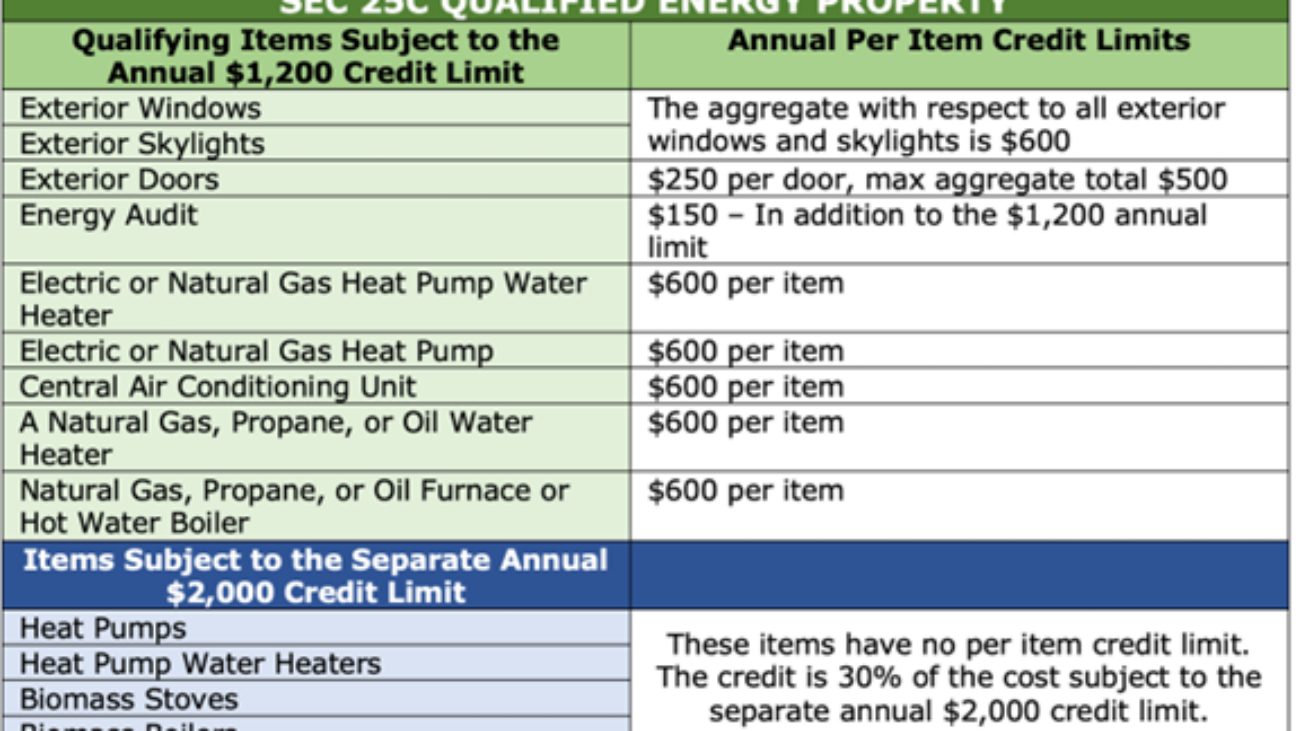

Navigating the complexities of real estate taxation can be daunting, especially when aiming to achieve the status of a Real Estate Professional under IRS guidelines. This designation is coveted among property owners and investors due to its potential to significantly reduce how passive activity losses are taxed. Let’s delve into what it means to be a real estate professional, the qualifications required, and the strategic decisions that can lead to tax efficiency.

Attaining the status of a real estate professional offers significant tax benefits, particularly regarding the treatment of passive activity losses. Typically, passive losses, such as those from rental real estate, can only offset passive income, limiting the ability to deduct them from other forms of income. However, as a qualified real estate professional, you can potentially convert these losses into active losses, allowing them to offset ordinary income, including wages and business profits. This can result in substantial tax savings, as it enables you to lower your taxable income effectively. Furthermore, this status can enhance tax planning flexibility, allowing for greater strategic management of income and investments. Ultimately, the designation not only aids in optimizing current tax liabilities but also supports long-term financial growth by preserving more capital for reinvestment and personal use.

Real estate professional status is also beneficial when considering the implications of the Net Investment Income Tax (NIIT), which imposes an additional 3.8% tax on net investment income for individuals earning above certain thresholds. Typically, rental income is classified as passive, making it subject to this surtax. However, real estate professional status can transform this rental income into non-passive income, thereby potentially exempting it from the NIIT.

This exemption is significant, especially for high-income property owners, as it reduces overall tax liability and preserves more of their rental income. By shielding rental income from the NIIT, real estate professionals can prevent erosion of returns due to this surtax, facilitating enhanced cash flow and greater reinvestment opportunities. Understanding and leveraging this status is, therefore, not only a tactical advantage but a pivotal element in strategic tax planning for property owners.

Achieving the designation of a real estate professional involves meeting specific IRS criteria, which help determine how your rental activities are taxed:

Qualifications for Real Estate Professional Status – To be classified as a real estate professional, you need to meet two primary criteria:

- Qualification #1 – More than half of the personal services you perform during that yearare performed in real property trades or businesses in which you materially participate, AND

- Qualification #2 – You perform more than 750 hours of services during that year in real property trades or businesses in which you materially participate.

Thus, a taxpayer who owns at least one interest in rental real estate and who meets the above tests is a real estate professional.

Achieving this requires diligent record-keeping to document hours spent on various activities such as property management, tenant relations, maintenance, and development. Let’s examine the tax meanings of these terms.

Definitions – the following are the definitions of the references included in the two qualifications:

- Personal Services – Means any work performed by an individual in connection with a trade or business, but not as an investor.

- Real Property Trade or Business – Is any real property development, redevelopment, construction, reconstruction, acquisition, conversion, rental, operation, management, leasing or brokerage trade or business. The determination of a taxpayer’s real property trades or businesses is based on all relevant facts and circumstances. Once a taxpayer determines the real property trades or businesses in which personal services are provided, they can’t redetermine them later unless the original determination was clearly erroneous or there’s been a material change of facts and circumstances

- Material Participation – Material participation is determined by assessing the depth and consistency of a taxpayer’s involvement in business operations. According to IRS guidelines, this signifies more than casual or sporadic participation, entailing regular, continuous, and substantial engagement in the real estate activities. The commitment to these activities must be significant enough to meet or exceed several specific IRS tests. These tests help ensure that the taxpayer plays a crucial role in the property’s management and decision-making processes, thereby distinguishing passive investors from those actively engaged in real estate operations.

- 500-Hour Test: Spend at least 500 hours per year on significant participation activities (SPAs), with each SPA requiring more than 100 hours individually.

- Substantially All Participation: Provide substantially all the participation in the activity throughout the tax year.

- 100-Hour Test: Spend more than 100 hours on the activity, ensuring no other individual spends more hours on it than the taxpayer.

- Aggregate Time Participation: Spend more than 500 hours across all significant participation activities, which include activities each undertaken for over 100 hours annually.

- Prior Participation: Materially participate in any five of the last ten taxable years or, for those in personal service businesses, participate materially in any three previous tax years.

Multiple Property Owners – IRS guidelines allow taxpayers to treat multiple rental properties as a single activity for tax purposes. This strategy is particularly beneficial for those aiming to qualify as a real estate professional, as it simplifies meeting the material participation requirements. By aggregating, instead of having to demonstrate involvement separately for each property, you can combine the hours spent across all properties, making it easier to meet the necessary thresholds for real estate professional status.

However, electing to aggregate comes with certain obligations and consequences. Once you choose to aggregate your rental activities, this decision is binding for all future tax years, meaning you must consistently report these properties as a single activity on subsequent returns. This can streamline tax reporting, but it also removes flexibility; if circumstances change or it becomes advantageous to separate these activities, your ability to do so is limited unless you can justify a change under specific IRS provisions.

Failing to elect aggregation when it would be beneficial or not adhering to the consistency requirement can lead to missed opportunities for tax savings and possible scrutiny in case of an audit. Therefore, it’s crucial to carefully consider the decision to aggregate, ensuring it aligns with your long-term investment strategy and tax planning goals. Proper documentation and adherence to IRS rules are essential to leverage the advantages of aggregation effectively.

As you can see, it difficult to qualify and maintain the status as a Real Estate Professional, but if you do qualify the tax benefits can be substantial. Contact this office with questions and for assistance in determining if you qualify.