Tennessee Tax Legislative Update

As previously shared through an earlier update, in January Governor Bill Lee announced plans to amend the Tennessee franchise tax to simplify the calculation. Under existing law, the franchise tax ba ...

Complete Elementor Demo - Phlox WordPress Theme

As previously shared through an earlier update, in January Governor Bill Lee announced plans to amend the Tennessee franchise tax to simplify the calculation. Under existing law, the franchise tax ba ...

Disabled individuals, as well as parents of disabled children, may qualify for several tax credits and other tax benefits. If you or someone listed on your federal tax return is disabled, you may be ...

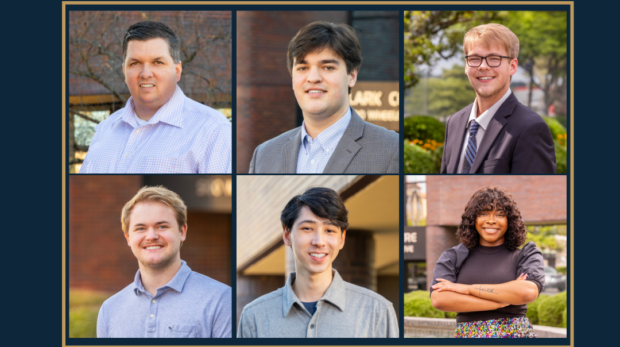

Internships offer a dynamic avenue for expanding your network and forging valuable connections. At RBG, interns collaborate directly with industry professionals, fostering relationships that can shape ...

There are some unique ways to make charitable contributions that can provide tax advantages to the donor. Before deciding about your charitable giving for the year, you may benefit from this article ...

Tax season can be stressful enough without having to worry about falling victim to tax scams. With cybercrime and identity theft becoming increasingly prevalent as more people file their taxes online ...

For many business owners, the future is uncertain. Would you like to ensure the long-term success of your enterprise, reducing stress and providing peace of mind? That’s where succession planning com ...

As the winds of economic uncertainty continue to blow, many businesses find themselves sailing through turbulent waters. With high-interest rates and mounting consumer debt, fears of an impending rec ...

As the current tax season continues, the Internal Revenue Service (IRS) has ushered in a new era of tax enforcement thanks to the power of artificial intelligence (AI). AI tools have taken nearly eve ...